From Germany to net-zero cost & much more

In this edition, we explore what is ailing Germany, while looking at the cost to attain net-zero along with India's success story of financial inclusion. We also discuss Apple's future and EU's DMA

Is Germany stalling big time?

From middle of 2000 till around 2010, Germany grew by 24% and was the shining star in Europe. During that time, the other growing countries within Europe was behind than Germany - UK was growing at 22% while France was around 18%. This has been a contrast to the current situation where ordinary citizens are unhappy with the government and the most vaunted economic model seems to be faltering.

Based on expert analysis, the immediate challenges facing Germany are in multiple fronts:

End of cheap Russian gas imports

China, who was one of the biggest trading partners for Germany, is now becoming a difficult market for German exporters

Germany is facing an ageing population and shrinking labour market, which is so significant for the famous German manufacturing sector

Lagging behind on the digital technologies with one of the poorest speeds in Europe, specially across western Europe

Spend on defense is likely to grow considerably, given the geo-political situation near its borders

While Germany has been consistent through their policy making of limiting their debts as compared to other countries, whether this fundamental policy can be potentially limiting growth is something to be watched, specially given their constraints and challenges the country is facing

Under the German “debt brake rule”, given that they had already taken a huge debt of around €500bn euros to address covid situation, their overall debt burden of ~60% of GDP is likely to go up to ~68% of GDP, much higher than the 60% limit set by the European Union.

As a result of their “debt brake” rule, which Germany will start again in 2024 (after one year of exception due to covid), the country is likely to taken on a mere €16.6bn debt in FY24.

However, with the global focus on readjusting the supply chains across the world & trying to reduce dependency with China, Germany has the opportunity to benefit from that. But that is likely to come with a price as countries are luring big corporations with tax subsidies and Germany is no exception - €10bn subsidy for Intel, €5bn for TSMC and so on.

How this rebalancing can be done without increasing debt levels and taxes, while keeping decent spending across sectors, remains to be seen.

As a result, IMF forecast that Germany will grow by around 8% till 2028, whereas other countries are likely to grow at a higher rate in the same period - France by 10%, Netherlands by 15% and US by 17%.

The cost to achieve net zero

Can you imagine a world of zero emission cars on the road, green energy providing power to our houses? While some say this is still a utopian dream, others feel that this is no longer an “option”, but something that has to be achieved to save our planet earth. However, the cost to achieve net zero is considerable:

The International Monetary Fund (IMF) estimates that the economic cost of achieving net zero emissions by 2030 would be 0.5% of global GDP. This is based on the assumption that countries cooperate on decarbonization and agree to price or tax carbon, while also scrapping current subsidies for fossil fuels. However, the IMF's estimates are based on hypotheticals that are not currently being met by countries. For example, the IMF assumes that there will be a global accord to price or tax carbon, but this has not yet been achieved.

The International Energy Agency (IEA) estimates that annual investment in decarbonization would need to rise from $2 trillion to almost $5 trillion by 2030. This would represent 2.5% of global GDP.

Another estimate puts the cost of decarbonization at an extra $3 trillion a year, or $100 trillion over 30 or 40 years. This would be used to boost renewable energy, electrify transport systems, decarbonize the heating and cooling of buildings, and foster green hydrogen.

New modelling by the Organisation for Economic Co-operation and Development (OECD) suggests that the fiscal cost of decarbonization would be higher than the IMF's projections. The OECD estimates that net public revenues would decline by 0.4% of GDP in 2030 and 1.8% of GDP in 2050.

In conclusion, the economic cost of achieving net zero emissions by 2030 is uncertain. Governments are facing a difficult choice: how to fund the green transition without raising taxes or cutting spending in other areas. On the one hand, borrowing costs are rising, and there is already a need for more spending on defense, pensions, and healthcare. On the other hand, the cost of inaction on climate change is also high.

The real question is not how much the green transition will cost, but how much more expensive it will be to do nothing.

Financial inclusion in India riding on digitisation

In the recently concluded G20 session in India, World Bank had come up with a document highlighting the impact of digitisation in India.

India has achieved around 80% financial inclusion rate. This was done in 6 years time. Without the digital payment infrastructure (bank accounts, aadhaar, mobile connectivity), India would have taken around 47 years to achieve the same milestone.

Total value of UPI transactions (digital inter-bank mobile based transactions) was around 50% of India’s nominal GDP.

“Banks’ costs of onboarding customers in India decreased from $23 to $0.1.

Banks that used e-KYC lowered their cost of compliance from $0.12 to $0.06

Because of the digital model, India did a total savings of $33 billion, equivalent to nearly 1.14% of GDP

Since its launch, the number of Pradhan Mantri Jan Dhan Yojana (PMJDY) accounts opened tripled from 147.2 million in March 2015 to 462 million by June 2022; women own 56% of these accounts, more than 260 million.

The account aggregator ecosystem has already triggered substantial productivity and business growth:

SME lending conversion has been 8% higher

65% savings in depreciation costs

66% reduction of costs related to fraud detection

India has built the world’s largest digital government-to-people architecture.

“This approach has supported transfers amounting to about $361 billion directly to beneficiaries from 53 central ministries through 312 key schemes. As of March 2022, this resulted in a total savings of $33 billion, equivalent to nearly 1.14% of GDP,”

US - China trade relationship with Apple in the middle

Amidst the ongoing “trade war” going between US and China, Apple has been handed a big blow to its business in China. As reported by the Wall Street Journal and Bloomberg, the Chinese government will be banning use of iPhone and other foreign devices for all central government workers. It is also likely to be extended to all state government workers as well. The impact for Apple might be considerable:

Out of 230 million iPhones shipped globally by Apple, a considerable amount is bought by around 56 million consumers in China, who works by state-owned units.

The latest restriction by China mirrors similar bans taken in the US against Chinese smartphone maker Huawei Technologies, who is likely to gain the most in the current scenario.

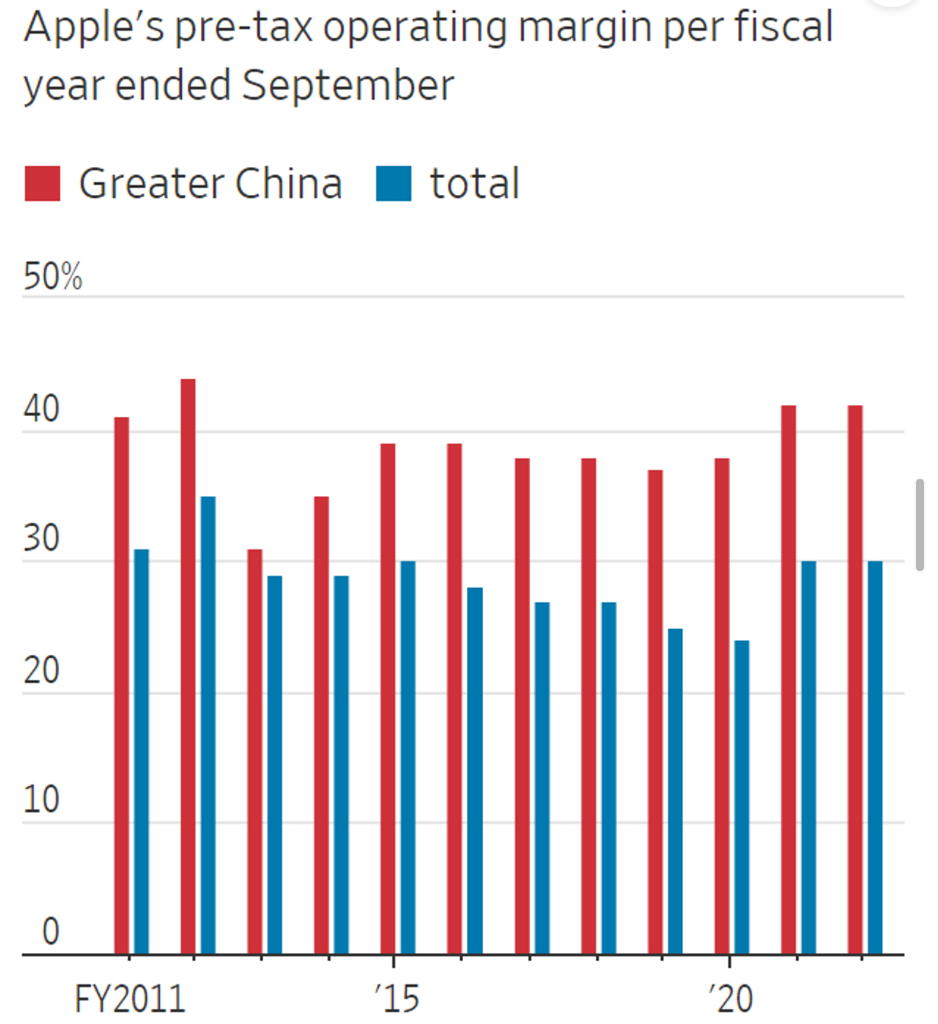

Traditionally, Apple's Greater China segment had pretax operating margins that were much higher than the company’s overall margins, with a clear 12 percentage points difference in last year. Hence, the impact of the total ban might have an impact on the overall margin in 2023 & beyond

In the short-term basis, Apple share prices dropped by 7% on a single day, when this news broke.

EU and Digital Markets Act (DMA)

In our earlier newsletter (link below), we had written about how the European Union is going all out to reign the powers of the big tech companies, while protecting the privacy of ordinary citizens.

The European Union has now named six tech giants who needs to be compliant to a new set of rules on how these gatekeepers can operate designated “core platform services”. The Digital Markets Act (DMA) has identified a total of 22 essential platform services that are operated by six dominant companies.

The DMA adopts a proactive approach to address competition concerns once these companies attain a certain level of market power, which is defined by:

Having more than 45 million active local users.

Achieving a turnover of over €7.5 billion in the past three financial years

Having a market capitalization exceeding €75 billion.

These gatekeeper firms now have a six-month period to adhere to the complete set of regulations and restrictions outlined in the DMA. This move aims to provide greater choices and increased freedom to both end users and businesses that rely on the services offered by these gatekeepers.

While Europe has triggered of clear actions protecting user privacies, it remains to be seen how the rest of the world reacts to this ever-growing concern.