From India to US this week

This week we focus majorly on India covering topics of chip making, nuclear power generation, offshore Rupee bonds & Russia's Rupee balance. We end with the ever-increasing US debts.

India focusing on chip making

The Indian government is currently in the process of assessing semiconductor proposals totaling $21 billion.

Among these, Israel's Tower Semiconductor Ltd. has presented a $9 billion plan for a manufacturing plant, while India's Tata Group has proposed an $8 billion chip fabrication unit.

Tata Group is anticipated to collaborate with Taiwan's Powerchip Semiconductor Manufacturing Corp. for its venture, though discussions have also taken place with United Microelectronics Corp.

Furthermore, Tata Group has outlined plans for a 250-billion-rupee ($3 billion) chip-packaging facility in eastern India, which will handle the assembly and export of chips, catering to various industries, including automakers like Tata Motors Ltd., which falls under the conglomerate's control.

In a strategic move, Japan's Renesas Electronics Corp. is exploring a partnership with Murugappa Group's CG Power and Industrial Solutions Ltd. arm to establish a chip-packaging facility.

As part of India's chipmaking incentive plan, the government is committed to covering half of the approved project costs, allocating an initial budget of $10 billion for this initiative.

This initiative has previously facilitated the establishment of a $2.75 billion assembly and testing facility in Gujarat by the U.S.-based memory maker, Micron Technology Inc.

India pivoting to nuclear power

India is set to extend invitations to private enterprises to contribute approximately $26 billion towards the development of its nuclear energy sector, with the primary objective of augmenting electricity production from eco-friendly sources devoid of carbon dioxide emissions.

This financial injection is crucial for India to reach its ambitious goal of ensuring that 50% of its total installed electric generation capacity relies on non-fossil fuels by the year 2030, marking a significant increase from the current 42%.

The anticipated influx of capital is envisioned to catalyze the establishment of 11,000 megawatts (MW) of nuclear power generation capacity by the year 2040.

Presently, the Nuclear Power Corp of India Ltd (NPCIL), a government-run entity, oversees and manages India's existing array of nuclear power plants, boasting a cumulative capacity of 7,500 MW. NPCIL has also committed investments for an additional 13,000 MW.

Under the proposed funding framework, private entities will play a pivotal role by investing in the nuclear plants, acquiring essential resources such as land and water, and spearheading construction activities in areas beyond the reactor complex.

However, in accordance with existing legal provisions, the rights to construct, operate, and manage the stations, as well as oversee fuel management, will remain vested in NPCIL.

It is anticipated that private companies will derive revenue from the sale of electricity generated by the power plants, while NPCIL will retain operational control, managing the projects for a specified fee.

This collaborative approach seeks to leverage both public and private expertise, fostering a sustainable and efficient expansion of India's nuclear energy infrastructure.

Demand for offshore India Rupee bonds soar

Global financial institutions, including the World Bank's lending arm, have successfully released offshore Rupee-denominated bonds, totaling $1.4 billion in the current year.

Notably, this year's bond issuance in the month of January represents almost half of the $3.3 billion recorded in the entirety of 2023.

This surge in issuance is attributed to heightened demand fueled by JP Morgan's announcement that India would become part of the Emerging Market Bond Index (EMBI) starting June 2024.

The offshore bonds, spanning maturities from 4 to 10 years, are denominated in Indian rupees but settled in U.S. dollars.

This financial instrument enables issuers to secure U.S. funds at more cost-effective rates, offering overseas investors entry into the Rupee debt market without the need for special onshore licenses or the obligation to pay local taxes.

Investment bankers highlight that these bonds serve as a straightforward channel for investors seeking to hold debt without establishing intricate local arrangements.

Additionally, other supranational entities with "AAA" ratings, such as the European Bank for Reconstruction & Development, Inter-American Development Bank, and the Asian Infrastructure Investment Bank, have also entered the market with Rupee-denominated bonds.

Key arrangers for these transactions include prominent institutions such as JP Morgan, Goldman Sachs, Standard Chartered Bank, and HSBC.

Russia’s Rupee balance

Russia has substantially utilized its Rupee balance, estimated to exceed $8 billion, residing in the special vostro accounts of Indian banks.

This balance, primarily accumulated through payments for Russian defense acquisitions, has been depleted across various channels.

These encompass expenditures on Indian imports, investments in infrastructure projects, participation in the equity market, and acquisition of government securities.

Despite the considerable utilization of the Rupee balance, particularly stemming from defense transactions, which constitute a significant portion of India's military hardware procurement, the government remains optimistic. It anticipates that future Rupee payments deposited into vostro accounts will continue to be strategically employed by Moscow through identified channels.

A noteworthy collaboration between India and Russia is the Vande Bharat deal, a joint venture aimed at manufacturing and maintaining 120 trains for the Indian Railways. The field of heavy engineering, integral to this venture, holds considerable potential.

In addition, reports from Russian media highlight an agreement involving the Goa shipyards in India, tasked with constructing 24 cargo ships for operation in the Caspian Sea. This initiative, set to be realized by 2027, features the active participation of the Russian Export Center.

The bilateral trade dynamics between India and Russia manifested a noteworthy surge in 2023, with Indian imports from Russia reaching $60.87 billion, marking a substantial 79 percent increase from the previous year. However, this surge resulted in a trade deficit of approximately $56 billion.

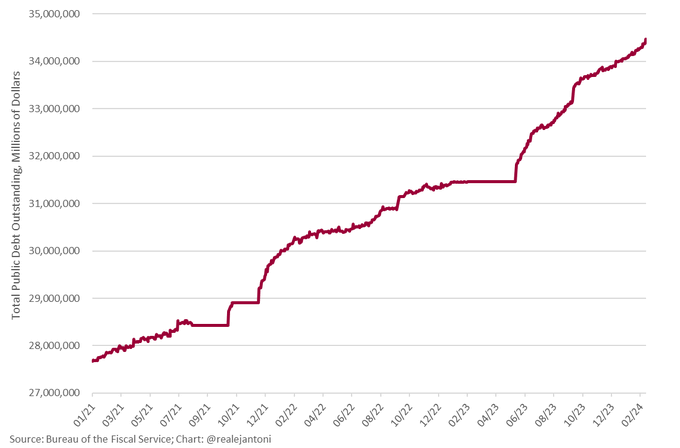

The ever-rising graph of US debt

As on 2nd March 2024, The United States' national debt has reached $34.471 trillion and is experiencing a consistent upward trajectory, increasing by $1 trillion approximately every 100 days.

The progression from $32 trillion to $33 trillion took 92 days, followed by the ascent from $33 trillion to $34 trillion in 106 days.

The current pace suggests that the transition from $34 trillion to $35 trillion is anticipated within the next 100 days.

Projections indicate a concerning trend, with the potential for the US national debt to escalate at a rate of $1 trillion per 30 days in the coming years.

This alarming development creates a precarious situation where the necessity to borrow additional funds becomes essential, primarily to meet the interest obligations associated with the existing debt.